A. PARTNERSHIP

WHAT IS IT?

Is a relationship between persons who have agreed to share profit and loss of the business carried by all with a profit meditative.

Partners: Are persons making an agreement to carry business for a common purpose/intention.

- Individual – these are partners (Persons by nature).

-

Collectively – This is a firm (legal persons).

MAIN FEATURES OF PARTNERSHIP;

edu.uptymez.com

- Two or more persons.

- There must be an agreement between partners.

- Lawful business.

- Profit Motive.

- Principal to agent relationship.

- Unlimited liabilities.

edu.uptymez.com

B.

CAPITAL ACCOUNTS

Capital can be contributed

(a) In kind

Anything equivalent to cash e.g. A house, a car etc

| ENTRIES | |

| DR ; Motor car A/c | |

| CR ; Capital A/c | |

| b) In cash | |

| – It is in cash | |

| ENTRIES | |

| DR ; Cash A/c | |

| CR ; Capital A/c | |

| c) Both cash and in kind | |

| – Partner brought part in cash and part in kind. | |

edu.uptymez.com

TYPES OF CAPITAL ACCOUNTS

There are two types of Capital Account

(a) Fluctuating capital Account

- Also it is known as floating capital account.

- This system partners capital account do not remain intact (as its original balance but fluctuates quite frequently)

- It means the capital account changes with all items concerning partners e.g. Interest on drawings, interest on capital, Partners salaries, commission, Drawings, Properties brought in, Profit and less nglish-swahili/distribution” target=”_blank”>distribution.

edu.uptymez.com

(b) Fixed Capital Account

Under this system the original capital invested by the partners remain unaltered unless additional capital is invested or capital itself is withdrawn by mutual agreement.

(c) Partner’s Current Account

It is an account that carries all items concerning Partners e.g. Interest on capital, Interest on drawings, Drawings, Partner’s salaries and wages/ commission to partner.

(d) Profit and Loss Appropriation Account

This is an extension of usual profit and loss Account, it Is prepared for adjusting transaction relating to the partnership deed.

Contents

- Interest on partner’s capital.

- Interest on partner’s drawings.

- Interest on partner’s loans.

- Partners salaries.

- Partner’s commission.

edu.uptymez.com

NOTE

These transactions are treated separately without mixing up with general trading transaction.

ENTRIES

| DR | CR | ||

| 1 | Interest on Partner’s Capital | ||

| DR; Interest or past Capital a/c | xx | ||

| CR; Partner’s capital (current a/c | xx | ||

| Transfer (fx) | |||

| DR; Profit and loss appropriation a/c | xx | ||

| CR; Interest on Partner’s capital | xx | ||

| 2 | Interest on drawings | ||

| DR; Partner’s Capital/Current a/c | xx | ||

| CR; Interest on Partner’s Drawings | xx | ||

| Transfer (fx) | |||

| DR; Interest on Partner’s Drawings a/c | xx | ||

| CR; Profit and loss Appropriation a/c | xx | ||

| 3 | Interest on Partner’s Loans | ||

| DR; Interest on Partner’s Loan | xx | ||

| CR; Partners capital a/c | Xx | ||

| Transfer (fx) | |||

| DR; Interest on partner’s Loan | xx | ||

| CR; | Xx | ||

| 4 | Partner’s salaries/Commissions | ||

| DR; Partner’s salaries/commission | xx | ||

| CR; Partner’s capital a/c | Xx | ||

| Transfer (fx) | |||

| DR; Profit and loss appropriation a/c | xx | ||

| CR; Partner’s salaries/commission | Xx | ||

edu.uptymez.com

EXERCISE 1

Amake and Babake started a partnership on 1st January, 2010. Both agreed in the partnership did the following;

- To contribute Shs.100, 000 each as capital.

- To share Profit and loss equally.

- Interest on capital at a rate of 5%.

- Interest on drawings at a rate of 10%.

- Partner’s salary Shs.50, 000 per month each.

edu.uptymez.com

Transactions for the Month of January, 2010

| 1st January,2010 | Invested required capital as per deed | |

| “ | Purchased goods from RTC | 700000 |

| “ | Purchased goods from Ally cash | 100000 |

| “ | Babake inject additional funds in cash | 200000 |

| “ | Amake took 50,000 shs from the firm to pay school fees for his son | |

| 31st January 2010 | Sold goods to NMC worth | 2,000,000 |

| Sold goods to NMC by cash | 500,000 | |

| Goods counted physically worth | 100,000 | |

| Paid rent | 10,000 | |

| Rent received | 100,000 | |

| Paid to partner’s January salaries | ||

| Paid salaries | 2000 | |

| Paid productive wages | 5000 |

edu.uptymez.com

Required

-Journal Proper to record all the transaction (No narration needed)

-Prepare ledger a/c’s to record all transactions relating to the months 1/2010

-Prepare trading profit and loss a/c and appropriation account for the period in a question.

-Show by extracting financial position of the A and B partnership (Amake and Babake).

PROFIT AND LOSS APPROPRIATION ACCOUNT

| Commission | xxx | Net profit b/d | Xxx |

| Net loss | xxx | interest on drawings | |

| partner’s salaries A- xx | A – xx | ||

| B – xx | xxx | B – xx | Xxx |

| Bonus to partner’s | |||

| Interest on loan xx | |||

| general reserve xx | |||

| Residual profit | |||

| A – xx | |||

| B – xx | xxx | ||

| xxxx | xxxx | ||

edu.uptymez.com

PROFIT APPORTIONMENT BASIS

We are having two Basis of Apportioning residual profits

- Time Basis Apportionment.

-

Profit analysis basis.

TIME BASIS APPORTIONMENT

edu.uptymez.com

In this method profit is apportioned between the various periods. That is to say the profit is accrued evenly.

Example

A and B are in partnership with share profit of .3:2 respectively on 1st January their capital stood at 500,000 and 400000 respectively. They decided to admit C as a new partner on 1st October, 2010, their new share profit ratio is 2.2.1. During the year the following Transaction took place.

| Tshs | ||

| Purchases were | 1,000,000 | |

| Sales were | 2,500,000 | |

| Partner’s salaries | 600,000 | |

| C brought 100,000 as capital | ||

| Interest on capital 10% p.a | ||

| Electricity | 100,000 | |

| Salaries and wages | 200,000 | |

edu.uptymez.com

Required;

-Prepare Profit and loss appropriation on time basis for A and B partnership and ABC partnership. Financial year ended 31st Dec. 2010:

Workings (W).

A AND B

PROFIT AND LOSS APPROPRIATION ACCOUNT FOR THE PERIOD ENDED

30TH SEPTEMBER, 2010

| (Trading) | (shs) | ||

| Purchases | 750,000.00 | sales | 1,875,000.00 |

| gross profit c/d | 1,125,000.00 | ||

| 1,875,000.00 | 1,875,000.00 | ||

| electricity | 75,000.00 | gross profit b/d | 1,125,000.00 |

| salaries and wages | 150,000.00 | ||

| net profit c/d | 900,000.00 | ||

| 1,125,000.00 | 1,125,000.00 | ||

| interest on capital | Net profit b/d | 900,000.00 | |

| A – 45,000 | |||

| B – 30,000 | 75,000.00 | ||

| Partner’s salary | 450,000.00 | ||

| residual profit | |||

| A – 225,000 | |||

| B – 150,000 | 375,000.00 | ||

| 900,000.00 | 900,000.00 | ||

edu.uptymez.com

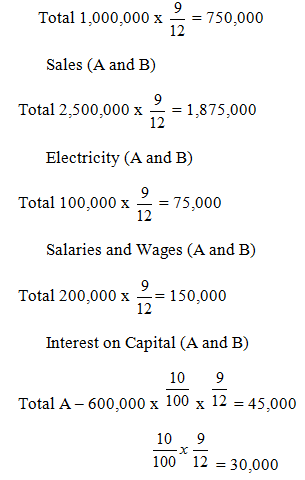

Working ; – W2purchases (A, B & C)

Total 1,000,000 x 9/12 = 250,000

Sales (A, B & C)

Total 2,500,000 x 9/12 = 625,000

Electricity (A, B &C)

Total 100,000 x 9/12 = 25,000

Salaries and wages (A, B & C)

Total 200,000 x 9/12= 50

Interest on capital (A, B & C)

Total A – 600,000 x10/100 x9/12 = 15,000

B – 400,000 x10/100 x 9/12= 10,000

C – 100,000 x x = 2500

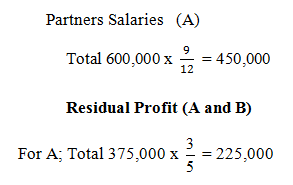

Partner’s salaries (A, B & C)

Total 600,000 x = 50,000

Residual value

For A; Total 123,500 x = 49,400

For B; Total 123,500 x = 49,400

For c; Total 123,500 x = 24,700

A, B & C PROFIT AND LOSS APPROPRIATION ACCOUNT FOR THE PERIOD END 30TH SEPT.

| (Trading) | shs | ||

| purchases | 250,000 | sales | 625,000 |

| gross profit c/d | 375,000 | ||

| 625,000 | 625,000 | ||

| electricity | 25,000 | gross profit b/d | 375,000 |

| salaries and wages | 50,000 | ||

| net profit c/d | 300,000 | ||

| 375,000 | 375,000 | ||

| net profit b/d | 300,000 | ||

| interest on capital | |||

| A – 15,000 | |||

| B – 10,000 | |||

| C – 2500 | 27500 | ||

| Partner salary | 150,000 | ||

| residual profit | |||

| A – 49,400 | |||

| B – 49,400 | |||

| C – 24,700 | 123,500 | ||

| 300,000 | 300,000 | ||