DEPRECIATIAON

Definition.

Is the decrease in value of assets or is the fall of value of Assets.

What factors causes Depreciation.

1) Physical deterioration or Tear and Wear, caused by sun, wind, duff resting, or frequent use of an asset and other weather element.

2) Economic factors. Asset becomes outdated even through it is in good physical condition.

3) Time factors. Physical economic factors caused by out dated or fashion out or style.

4) Depletion factors. Natural resources, mining’s, oil wells.

5) Amortization factors. Introduce Goodwill, trademarks, copyrights.

METHODS OF CALCULATING DEPRECIATION.

There are three method of calculating Depreciation, These are:-

1) Straight line method/equal installment/ cost price.

2) Diminishing balance method or declining OR reducing balance method.

3) Revaluation.

1. STRAIGHT LINE METHOD.

Equal amount of an asset charged each year for Depreciation.

OR

Using this method, certain percentage of the original cost of the asset is taken in a year.

The money amount is the depreciation for the years and the cost of the fixed asset less the total depreciation is equal to the net book value.

Example.

A machine is purchased for TSHS 6,000 on 1 June 2000. It is to be depreciation by the straight line method at 10% each year. The firm financial year end at 31 December.

Calculation of Depreciation.

=cost price x10/100=600

The depreciation for each year is 600.

|

Cost price at 1st January 2000 |

|

6,000 |

||

|

less: |

Depreciation for Dec2000 |

|

600 |

|

|

|

|

|

|

5,400 |

|

less: |

Depreciation for Dec2001 |

|

|

600 |

|

|

|

|

|

4,800 |

|

less: |

Depreciation for Dec2002 |

|

|

600 |

|

Net book value at 31/12/2002 |

|

4,200 |

||

edu.uptymez.com

2. DIMINISHING / REDUCING BALANCE METHOD.

Amount of Depreciation charged according to the book value of the assets.

With this method a certain percentage of the money reduced (or diminishing) balance of start of each year is taken as the depreciation for the year.

Example.

A machine is purchased for Tshs 6000 on 1st January 1991. It is to be depreciation by the reducing balance method at 12% each year. The firm financial years end 31st December.

The machines will depreciate follows.

|

Cost at 1st 1991 |

6,000 |

|

Less: Depreciate for 1991 (12% of 6000) |

720 |

|

Book of values at 31st Dec 1991 |

5,280 |

|

Less: Depreciation for 1995(12% of 5280) |

634 |

|

Book of value 31st Dec 1992 |

4,646 |

|

Less: Depreciation 1993 (125of 4646) |

558 |

|

Book of value of 31 Dec 1993 |

4,088 |

edu.uptymez.com

NOTE.

The reducing balances method provides decreasing amount of depreciation each year in the second year the amount is less than in first in the third year it is less than the second year and so on.

3. REVALUATION METHOD OF DEPRECIATION.

The two previous method of calculation depreciation applied a certain percentage each year either to the cost of asset (straight line method) or to the reduced balance.

A third method for calculating depreciation is to value the fixed assets each year and the result fall in values during the year is the amount of depreciation for that year.

Example.

Office equipment is bought for Tshs 2,000 on 1st January 1995 it is devalued as follows.

31st December 1995 Tshs 1,600

31st December 1996 Tshs 1,350

31st December 1997 Tshs 1,000

Therefore depreciation amount will be; – for 1995 ……………………..Tshs 400

1996 ……………………..Tshs 250

1997 ……………………..Tshs 350

NOTE.

The revaluation method is often used for low cost fixed assets such as stock of work store tools or small items of office equipments which are frequently added during the year end.

Other methods may include the following;-

METHODS OF RECORDING FOR DEPRECIATION

A. NEW METHOD/ MODERN METHOD.

-Always fixed assets shown at cost prices remain constant fixed.

-Amount of depreciation accumulated to provision for depreciation a/c.

-Only amount of depreciation for current charged to profit or loss a/c.

-Always fixed assets shown at cost price.

B. OLD METHOD.

Example.

A machine in purchased for Tshs 2,000 on 1st January 1991. It is to be depreciated by the straight line method at 10% each for three years..

|

edu.uptymez.com

edu.uptymez.com

edu.uptymez.com

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

edu.uptymez.com

EXERCISE

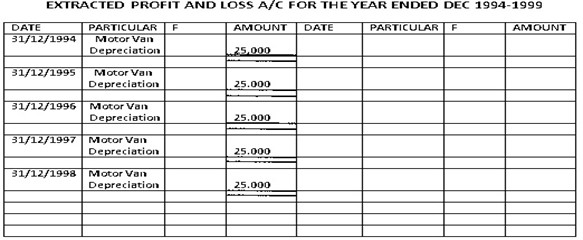

1994 bought motor van costing 2,000,000 depreciation is to be charged at the rate of 5% per annum using straight line method for five years respectively.

|

edu.uptymez.com

edu.uptymez.com

edu.uptymez.com |

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

edu.uptymez.com

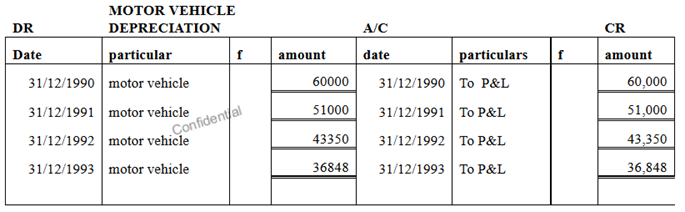

Example 2

A motor vehicle was bought on 1st January 1990 at cash price of 400,000. The company decide to depreciate the vehicle by 15% per annum using diminishing balance method for four years.

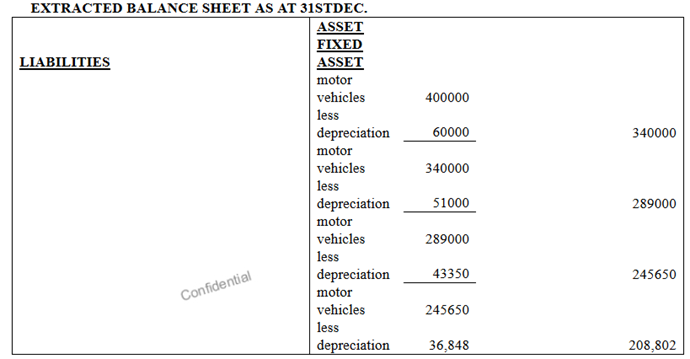

Your required to show relevant A/C and extracted balance sheet for four years.

WORKING;-

|

Motor vehicle at cost |

400,000 |

||

|

Less depreciation 31/12/90 – (400000 15/100) |

60,000 |

||

|

Balance of motor vehicle at book |

value |

|

340,000 |

|

Less depreciation 31/12/1991 (340,000 115/100) |

51,000 |

||

|

Balance of motor vehicle at book value |

|

289,000 |

|

|

Less depreciation 31/12/1992 (289000 15/100) |

43,350 |

||

|

Balance of motor vehicle at book value |

|

245,650 |

|

|

Less depreciation 31/12/1993 (245650 15/100) |

36,848 |

||

|

Balance of motor vehicle at book value. |

|

208,802 |

|

edu.uptymez.com

|

DR |

|

MOTOR VEHICLE |

A/C |

|

|

CR |

|

|

Date |

particulars |

f |

Amount |

date |

particulars |

f |

amount |

|

1/1/1990 |

cash |

|

400,000 |

31/12/1990 |

Depreciation |

|

60,000 |

|

|

|

|

|

31/12/1990 |

balance c/d |

|

340,000 |

|

|

|

|

400,000 |

|

|

|

400,000 |

|

1/1/1991 |

balance b/d |

|

340,000 |

31/12/1991 |

Depreciation |

|

51,000 |

|

|

|

|

|

31/12/1991 |

balance c/d |

|

289,000 |

|

|

|

|

340,000 |

|

|

|

340,000 |

|

1/1/1992 |

balance b/d |

|

289,000 |

31/12/1992 |

Depreciation |

|

43,350 |

|

|

|

|

|

31/12/1992 |

balance c/d |

|

245,650 |

|

|

|

|

289,000 |

|

|

|

289,000 |

|

Jan-93 |

balance b/d |

|

285,650 |

31/12/1993 |

Depreciation |

|

36,848 |

|

|

|

|

|

31/12/1993 |

balance c/d |

|

208,802 |

|

|

|

|

545,650 |

|

|

|

545,650 |

|

31-Jan |

balance b/d |

|

208,802 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

edu.uptymez.com

EXERCISE

The general Emma has PLANT AND MACHINE as on asset bought at 30th June 1995 for cash 700,000 came to you and ask you to help him to show the depreciate of that asset in relevant account statement . The depreciation method is reducing balance method at not of 20% for four years.

WORKING

|

PLANT AND MACHINE at cost |

|

|

|

700,000 |

|

Less depreciation 31/12/1995 (700000 ×20/100× ½) |

|

70,000 |

||

|

Balance of machine at book value |

|

|

630,000 |

|

|

Less depreciation 31/12/1996 (630000× 20/100× ½) |

|

63,000 |

||

|

Balance of machine and plant at the book value |

|

567,000 |

||

|

Less depreciation 31/12/1997 (567000 ×20/100× ½) |

|

56,700 |

||

|

Balance of plant and machine at book value |

|

510,300 |

||

|

Less depreciation 31/12/1998 (510300× 20/100× ½) |

|

51,030 |

||

|

Balance plant and machine of book value |

|

|

459,270 |

|

edu.uptymez.com

DR PLANT AND MACHINE A/C CR

|

Date |

Particulars |

amount |

dates |

particulars |

f |

amount |

|

1/6/1995 |

cash |

700000 |

31/12/1995 |

Depreciation |

|

70,000 |

|

|

|

|

31/6/95 |

balance c/d |

|

126,000 |

|

|

|

700,000 |

|

|

|

100,800 |

|

1/7/1996 |

balance b/d |

630000 |

31/07/1996 |

Depreciation |

|

126,000 |

|

|

|

|

31/07/1996 |

balance c/d |

|

504,000 |

|

|

|

630000 |

|

|

|

630,000 |

|

1/8/1997 |

balance b/d |

504,000 |

31/08/1997 |

depreciation |

|

100,800 |

|

|

|

|

31/08/1997 |

balance c/d |

|

403,200 |

|

|

|

567,000 |

|

|

|

504,000 |

|

1/9/1998 |

balance b/d |

403,200 |

31/9/98 |

Depreciation |

|

80,640 |

|

|

|

|

31/9/98 |

balance c/d |

|

322,560 |

|

|

|

|

|

|

|

403,200 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

edu.uptymez.com

DR DEPRECIATION FOR PLANT AND MACHINE A/C CR

|

Date |

particulars |

Amount |

Date |

Particulars |

f |

Amount |

|

31/6/95 |

Plant and machines |

70,000 |

31/12/1995 |

To p&L a/c |

|

70,000 |

|

31/07/1996 |

Plant and machines |

126,000 |

31/07/1996 |

To p&L a/c |

|

126,000 |

|

31/08/1997 |

Plant and machines |

100,800 |

31/08/1997 |

To p&L a/c |

|

100,800 |

|

31/9/98 |

Plant and machines |

80,640 |

31/09/1998 |

To p&L a/c |

|

80,640 |

|

|

|

|

|

|

|

|

edu.uptymez.com

|

|

||||

|

31/6/95 |

Depreciation Plant machine |

700,000 |

|

|

|

31/07/96 |

depreciation Plant machine |

126,000 |

|

|

|

31/08/98 |

depreciation Plant machine |

100,800 |

|

|

|

31/9/99 |

depreciating Plant machine |

80,640 |

|

|

|

|

|

|

|

|

edu.uptymez.com

EXTRACTED BALANCE SHEET AS AT 1995

|

|

LIABILITIES |

|

|

ASSETS |

|

|

|

|

|

|

|

FIXED ASSETS |

|

|

|

|

|

|

1995 |

Plant and machine |

700,000 |

|

|

|

|

|

|

less: depreciation |

70,000 |

630,000 |

|

|

|

|

1996 |

Plant and machine |

630000 |

|

|

|

|

|

|

less: depreciation |

126,000 |

504,000 |

|

|

|

|

1997 |

Plant and machine |

504,000 |

|

|

|

|

|

|

less: depreciation |

100,800 |

403,800 |

|

|

|

|

1998 |

Plant and machine |

403,200 |

|

|

|

|

|

|

less: depreciation |

51030 |

322,560 |

|

|

|

|

|

|

|

|

edu.uptymez.com

QUIZ

On 1/1/1989 bought furniture costing 150,000 depreciation to be at the rate of 13 1/3 % per annum using straight line method for three years.

DR FURNITURE A/C CR

|

DATE |

PARTICULARS |

AMOUNT |

DATE |

PARTICULARS |

|

AMOUNT |

|

1/1/1989 |

cash |

150,000 |

31/12/1989 |

depreciation |

|

20,000 |

|

|

|

|

31/12/1989 |

balance c/d |

|

130,000 |

|

|

|

150,000 |

|

|

|

150,000 |

|

1/1/1990 |

balance b/d |

130,000 |

31/12/1990 |

depreciation |

|

20,000 |

|

|

|

|

31/12/1990 |

balance c/d |

|

110,000 |

|

|

|

130,000 |

|

|

|

130,000 |

|

1/1/1991 |

balance b/d |

110,000 |

31/12/1991 |

depreciation |

|

20,000 |

|

|

|

|

21/12/1991 |

balance c/d |

|

90,000 |

|

|

|

110,000 |

|

|

|

110,000 |

|

1.1/92 |

balance b/d |

90,000 |

|

|

|

90,000 |

edu.uptymez.com

DR DEPRECIATION OF FURNITURE A/C CR

|

Date |

F |

particulars |

Amount |

date |

particulars |

f |

amount |

|

31/12/1989 |

|

furniture |

20,000 |

31/12/1989 |

P&L A/C |

|

20,000 |

|

31/12/1990 |

|

furniture |

20,000 |

31/12/1990 |

P&L A/C |

|

20,000 |

|

31/12/1991 |

|

furniture |

20,000 |

31/12/1991 |

P&L A/C |

|

20,000 |

|

31/12/1992 |

|

furniture |

20,000 |

31/12/1992 |

P&L. A/C |

|

20000 |

edu.uptymez.com

|

DR PROFIT AND LOSS ACCOUNT ASSET FOR THE YEAR ENDED 31 12 1989 CR |

||||

|

31/12/1989 |

Depreciation furniture |

20,000 |

|

|

|

31/12/1990 |

Depreciation furniture |

20,000 |

|

|

|

31/12/1991 |

Depreciation furniture |

20,000 |

|

|

|

31/12/1992 |

Depreciating furniture |

20,000 |

|

|

|

|

|

|

|

|

edu.uptymez.com

BALANCE SHEET AS AT 31 12 1989

|

|

LIABILITIES |

|

|

ASSETS |

|

|

|

|

|

|

|

FIXED ASSETS |

|

|

|

|

|

|

1989 |

FURNITURE |

150,000 |

|

|

|

|

|

|

less: Depreciation |

20,000 |

130,000 |

|

|

|

|

1990 |

FURNITURE |

130,000 |

|

|

|

|

|

|

less: Depreciation |

20,000 |

110,000 |

|

|

|

|

1991 |

FURNITURE |

110,000 |

|

|

|

|

|

|

less: Depreciation |

20,000 |

90,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

edu.uptymez.com