Solution.QN2

PURCHASES DAY BOOK/ PURCHASES JOURNAL

|

DATE |

PARTICULARS |

F |

INVOICE DETAILS |

INVOICE TOTAL |

|

|

1st May 4th May 8th May 15th May 26th May 30th May |

NATIONAL DISTRIBUTORS LTD – 10 bags of beans @ T.shs. 600 GEFCO – 2 dozen of cooking oil of @ T.shs. 50 KILIMANJARO TEXTILES – 10 dozen of bed sheet @T.shs. 2,200 GEFCO – 100 dozen of baby milk @ T.shs 600 KILIMANJARO TEXTILES – 20 dozen bed sheet @ T.shs. 2,200

Transfer purchases a/c by Dr in General ledger |

|

|

6,000 100 22,000 60,000 44,000

edu.uptymez.com |

edu.uptymez.com

MSTITU’S

PURCHASES RETURNS DAY BOOK / RETURNS OUTWARDS

|

DATE |

PARTICULARS |

F |

INVOICE DETAILS |

INVOICE TOTAL |

|

10th May 20th May 25th May 28th May

30th May |

NATIONAL DISTRIBUTORS LTD – 1 bags of beans @ T.shs. 600 GEFCO – ½ dozen of cooking oil of @ T.shs. 50 KILIMANJARO TEXTILES – 1 dozen of bed sheet @T.shs. 2,200 GEFCO – 5 dozen of baby milk @ T.shs 600 KILIMANJARO TEXTILES – 5 dozen bed sheet @ T.shs. 2,200

|

G.L |

|

2,200 |

edu.uptymez.com

PURCHASES LEDGERS

DR NATIONAL DISTRIBUTORS LTD CR

|

DATE |

DETAILS |

F |

AMOUNT |

DATE |

DETAILS |

F |

AMOUNT |

|

1st May |

Purchases returns |

|

6000 |

1st May |

purchases |

|

6,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

edu.uptymez.com

DR GEFCO A/C CR

|

DATE |

DETAILS |

F |

AMOUNT |

DATE |

DETAILS |

F |

AMOUNT |

|

10th May |

Purchases returns |

|

25 |

4th May |

purchases |

|

100 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

edu.uptymez.com

DR KILIMANJARO TEXTILES A/C CR

|

DATE |

DETAILS |

F |

AMOUNT |

DATE |

DETAILS |

F |

AMOUNT |

|

20th May |

Purchases returns |

|

2,200 |

8th May |

purchases |

|

22,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

edu.uptymez.com

DR GEFCO A/C CR

|

DATE |

DETAILS |

F |

AMOUNT |

DATE |

DETAILS |

F |

AMOUNT |

|

25th May |

Purchases returns |

|

3,000 |

1st May |

purchases |

|

60,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

edu.uptymez.com

DR KILIMANJARO TEXTILES A/C CR

|

DATE |

DETAILS |

F |

AMOUNT |

DATE |

DETAILS |

F |

AMOUNT |

|

28th May |

Purchases returns |

|

11,000 |

26th May |

purchases |

|

44,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

edu.uptymez.com

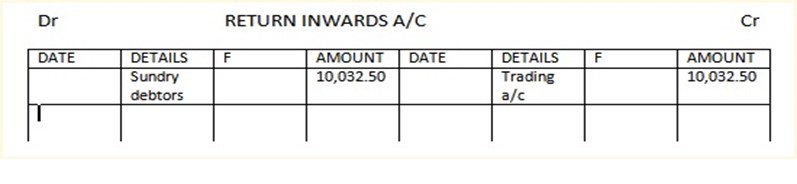

GENERAL LEDGERS

RETURN INWARDS JOURNAL OR SALES RETURN DAY BOOK

When goods are returned by the customer to the supplier a CREDIT NOTE Is issued by the supplier to the customers informs the customer that his account has been dully CREDITED .

A record of the returns of goods sold or credit is kept in returns inwards journal. They are immediately posted to the credit side of the customer’s account in the sales ledger and the total at returns- inwards is debited in the returns inwards account in the general ledger.

NOTE

A customer send a debit note to the supplies when the returned goods and the supplies issued a credit note to indicate that the customers account has been credited by the supplier.

EXAMPLES

The following are the returns inwards.

3rd Apr Mvita returned 2 dozen vitenge @ T.shs. 800, a dozen point by rain.

11th Apr issued a credit note to Said Ltd for goods retuned

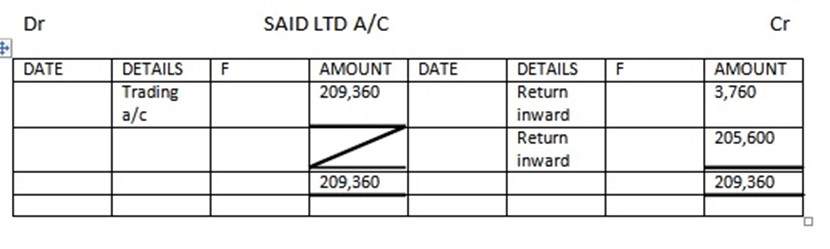

5 bag ammonium sulphate @ T.shs. 680 under weight

30 gallon bags @ T.shs 12, wrong size

14th April Mkali returned

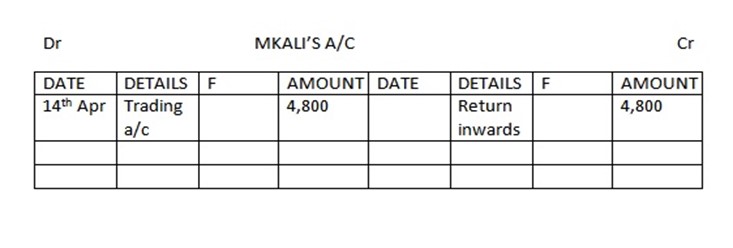

10 dozen stencil @ 300 wrong size

12 reams duplicating paper @ 150 wrong size

25th Apr return from Said Ltd

200 bags of maize @ T.shs 1,000 dully expired

40 bags of grand nuts @ T.shs. 140, dully expired

SALES RETURNS JOURNAL

(RETURNS INWARD BOOKS)

|

DATE |

PARTICULARS |

F |

INVOICE DETAILS |

INVOICE TOTAL |

|

3rd Apr 11th Apr 14th Apr 30th Apr |

MVITA – 2 dozen vitenge @ T.shs. 800 SAID LTD – 5 bag ammonium sulphate @ T.shs. 680 – 30 gallon bags @ T.shs 12 MKOLI – 10 dozen stencil @ 300 – 12 reams duplicating paper @ 150 SAID LTD – 200 bags of maize @ T.shs 1,000 – 40 bags of grand nuts @ T.shs. 140

|

|

360

1,800 5,600

|

1,600 3,760

4,800

205,600 215,760

|

edu.uptymez.com

SALES LEDGERS.

DR MVITA A/C CR

|

DATE |

DETAILS |

F |

AMOUNT |

DATE |

DETAILS |

F |

AMOUNT |

|

|

Trading a/c |

|

1,600 |

3rd Apr |

Sales returns |

|

1,600 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

edu.uptymez.com

EXERCISE.1

Records the following transaction in sales returns day book and then opened the necessary ledger Accounts.

2nd May A credit note was sent to S. Sandala for goods returned by him @ T.shs.12.50, wrong types.

3rd May returns at goods by H. Hasan Tshs. 91.5 hot according to order on the sasesh date a credit note was sent to L. Lowe for goods returns by him T.shs. 105 damaged in transist.

9th May B. Mlowe received a credit note for goods returns by him worth Tshs. 1,200 not of the sample

13th May A credit note was sent to C. Chande for goods returned by him 2100 wrong size.

15th May M. Pili was given a credit note for good value @ T.shs. 1,600 returned due to bad condition.

21st May returns of goods by C. Changula T.shs. 1,100 these were received in bad condition.

31st May N. Titto get a credit note for returns of goods by him worth Tshs. 3,000 not on the sample.

Solution.QN1

SALES RETURNS JOURNAL

|

DATE |

Particulars |

F |

Invoice details |

Invoice Total |

|

2nd May

9th May 13th May 15th May

21st May 31st May

|

S. SANDARA – goods returned by him @ T.shs.12.50 H. HASAN – According to order on the sasesh 915 B. MLOWE Goods returns by him worth T.shs.1,200 C. CHANDE – for goods returned by him 2,100

– was given a credit note for good value @ T.shs. 1,600 C. CHANGULA Goods in received in bad condition. T.shs. 1,100 N. TITTO credit note for returns of goods by him worth T.shs. 3,000

transfer the total to sale returns a/c

|

|

|

12.50 1,020 1,200 2,100

1,600 1,100

3,000 |

edu.uptymez.com

SALES LEDGER

DR S. SANDARA A/C CR

|

DATE |

DETAILS |

F |

AMOUNT |

DATE |

DETAILS |

F |

AMOUNT |

|

|

|

|

|

2nd May |

Sales returns |

|

12.50 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

edu.uptymez.com

GENERAL LEDGER

DR H. HASAN ACCOUNT CR

|

DATE |

DETAILS |

F |

AMOUNT |

DATE |

DETAILS |

F |

AMOUNT |

|

|

|

|

|

|

3rdMay |

Sales returns |

|

1,020 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

edu.uptymez.com

DR B. MLOWE ACCOUNT CR

|

DATE |

DETAILS |

F |

AMOUNT |

DATE |

DETAILS |

F |

AMOUNT |

|

|

|

|

|

9th May |

Sales returns |

|

1,200 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

edu.uptymez.com

DR C. CHANDE ACCOUNT CR

|

DATE |

DETAILS |

F |

AMOUNT |

DATE |

DETAILS |

F |

AMOUNT |

|

|

|

|

|

13th May |

Sales returns |

|

2,100 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

edu.uptymez.com

DR M. PILI ACCOUNT CR

|

DATE |

DETAILS |

F |

AMOUNT |

DATE |

DETAILS |

F |

AMOUNT |

|

|

|

|

|

13th May |

Sales returns |

|

1,600 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

edu.uptymez.com

DR C. CHANGULA ACCOUNT CR

|

DATE |

DETAILS |

F |

AMOUNT |

DATE |

DETAILS |

F |

AMOUNT |

|

|

|

|

|

21th May |

Sales returns |

|

1,100 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

edu.uptymez.com

DR N.TITTO ACCOUNT CR

|

DATE |

DETAILS |

F |

AMOUNT |

DATE |

DETAILS |

F |

AMOUNT |

|

|

|

|

|

31st May |

Sales returns |

|

3,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

edu.uptymez.com

EXAMPLE.1

A Raw land has the following purchases and sales for the March 1995

1st Mar Bought from Smith store silk 40, cotton 80 and less 25 percent trade discount.

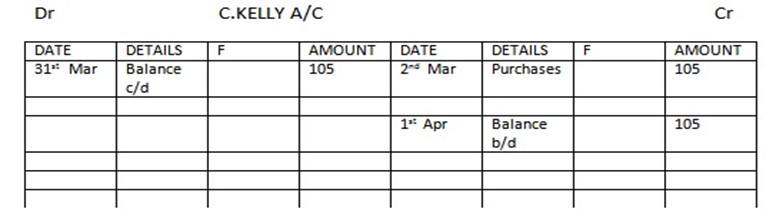

8th March Sold to C. KELLY they him goods 28 woollen item 44 No trade discount

15th Mar Sold to A. HENRY silk T.shs. 33 linen 44, cotton goods 120 all less 20% Trade discount

23rd Mar Bought from C. Kelly cotton shs. 88, linen shs. 52 all less 25% trade discount.

24th Mar Sold to D. SANCRESTER linen goods . 42, cotton 48 less 10 percent trade discount

31st Mar Bought from J. Hamitton linen goods 270 less 23 ½ percent trade discount

Required :

(a) Prepare purchases and sales journal of Raw land from above

(b) Post the item to personal Account

(c) Post the total of the journal to the sales and purchases Account.

Solution

RAW LAND’S

PURCHASES DAY BOOK

|

DATE |

Particulars |

F |

Invoice details |

Invoice Total |

|

1st Mar 2nd Mar 31st Mar

|

SMITH STORE Silk……………….40 Cotton……………80 Less 25% 120 trade discount C KELLY Cotton 88 Linen 52 Less 25% 140 trade discount J. HAMILTON Liner goods……..270 Less: 33 1/3 % of 270 trade discount.

Transfer the total to purchases A/c by Dr in General ledger

|

|

40 80 88 52 35 270 90

|

180 375 |

edu.uptymez.com

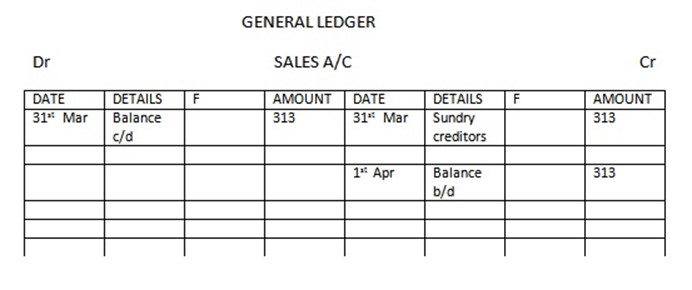

RAW LAND

SALES DAY BOOK

|

DATE |

Particulars |

F |

Invoice details |

Invoice Total |

|

8th Mar 15th Mar 24th Mar 31st Mar |

GRANTLEY Line goods 28 woollen item 44 A. HENRY Silk goods 36 Linen goods 44 Cotton goods 120 Less 20% of 200 trade discount. D. SANGSTER Linen goods 42 Cotton good 48 Less 10% of 90 trade discount Transfer the total to sales A/c by Cr in crv Ledger |

G.R |

28 44 36 44 120 – 40 42 48 90

|

72 160

81 313 |

200

200edu.uptymez.com

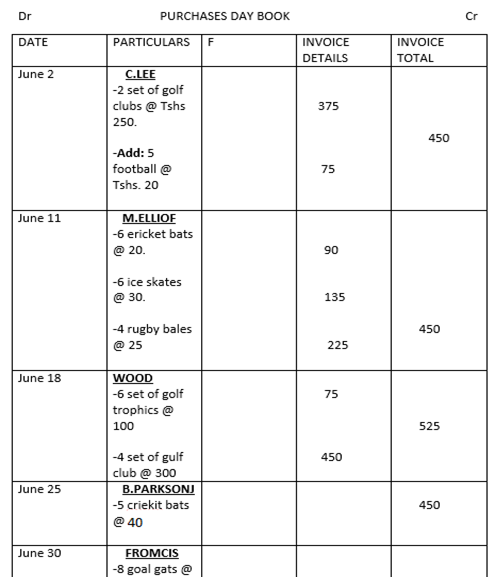

EXERCISE.1

C . Philips has the following purchases for the month of June 2002

June 2 from C. Lee 2 sets of golf clubs @ T.shs. 250

5 football @ T.shs. 20

Less 25 percent trade discount

June 11 From M. Elliot 6 ericket bats @ 20

6 ice skates @30

4 rugby bales @ 25

Less 25 percent trade discount

June 18 from wood

6 set of golf trophics @ 100

4 set of gulf club @ 300

Less 33 1/3 percent trade discount

June 25 From B. Parksons. 5 criekit bats @ 40

Less 25 percent trade discount

June 30 From fromeis 8 goal gasts @ 70

Less 25 percent trade discount

Required;

(a) Enter of the purchases journal for the month

(b) post the item to the supplier Account

(c) transfer the total to the purchases Accounts.

Solution.QN1

PURCHASES LEDGERS.

DR C. LEE ACCOUNT CR

|

DATE |

DETAILS |

F |

AMOUNT |

DATE |

DETAILS |

F |

AMOUNT |

|

|

|

|

|

2nd Jul |

purchases |

|

450 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

edu.uptymez.com

DR M. ELLIOF ACCOUNT CR

|

DATE |

DETAILS |

F |

AMOUNT |

DATE |

DETAILS |

F |

AMOUNT |

|

|

|

|

|

11th Jul |

purchases |

|

450 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

edu.uptymez.com

DR WOOD ACCOUNT CR

|

DATE |

DETAILS |

F |

AMOUNT |

DATE |

DETAILS |

F |

AMOUNT |

|

|

|

|

|

18th Jul |

purchases |

|

525 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

edu.uptymez.com

DR B. PARKSON ACCOUNT CR

|

DATE |

DETAILS |

F |

AMOUNT |

DATE |

DETAILS |

F |

AMOUNT |

|

|

|

|

|

25th Jul |

purchases |

|

450 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

edu.uptymez.com

DR FROMCIS ACCOUNT CR

|

DATE |

DETAILS |

F |

AMOUNT |

DATE |

DETAILS |

F |

AMOUNT |

|

|

|

|

|

30th Jul |

purchases |

|

420 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

edu.uptymez.com

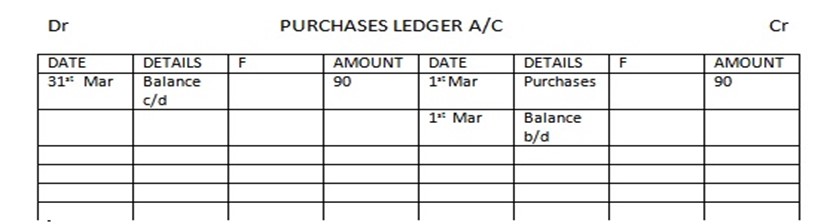

GENERAL LEDGER.

DR PURCHASES A/C CR

|

DATE |

DETAILS |

F |

AMOUNT |

DATE |

DETAILS |

F |

AMOUNT |

|

31thJul |

Sundry creditors |

|

2,290 |

31thJul |

Trading a/c |

|

2,290 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

edu.uptymez.com